本文首发于智堡公众号:zhi666bao。

新常态下通货膨胀与就业的脱节

It is a pleasure to be here at the National Tax Association Annual Spring Symposium. Just as it may take the tax experts and practitioners here today some time to disentangle the longer-term implications of recent major changes to tax policy, so, too, we are in the process of analyzing the lessons for monetary policy of apparent post-crisis changes in the relationships among employment, inflation, and interest rates

很高兴来参加国家税务协会主办的年度春季研讨会。正如今天的税务专家和从业人员可能需要一段时间来解决近期税收政策的重大变革所造成的长期影响,美联储也正在分析危机后货币政策的教训——就业,通货膨胀和利率之间关系的变化。

The Congress has assigned the Federal Reserve the job of using monetary policy to achieve maximum employment and price stability. Price stability means moderate and stable inflation, which the Federal Reserve has defined to be 2 percent inflation. Maximum employment is understood as the highest level of employment consistent with price stability. In the aftermath of the Great Recession, which had deep and persistent effects, it is important to understand whether there have been long-lasting changes in the relationships among employment, inflation, and interest rates in order to ensure our policy framework remains effective.

国会赋予了美联储使用货币政策来实现充分就业以及价格稳定的工作。价格稳定意味着温和而稳定的通胀,美联储已将其定义为2%的通胀目标。充分就业被理解为与价格稳定一致的最高就业水平。在经历了深刻且影响颇为持久的大萧条后,重要的是要了解就业,通货膨胀和利率之间的关系是否存在长期变化,以确保我们的政策框架持续有效。

就业和通货膨胀

This expansion will soon become the longest on record in the United States. Growth has persisted throughout the past decade, overcoming downdrafts from abroad and pullbacks in fiscal support earlier in the expansion and benefiting last year from a large fiscal boost. Recent data confirm that consumers remain confident, workers are productive, and businesses are hiring, although trade conflict is creating uncertainty.

本轮经济扩张很快将成为美国有史以来最长的一次。在过去十年中,美国经济持续增长,克服了国外经济下行的态势以及前期经济扩张期时财政支持的消褪,并从去年的大幅度财政刺激政策中受益。最近的数据证实,尽管贸易冲突带来了不确定性,但消费者仍然充满信心,工人们富有产效,而企业也在积极招聘。

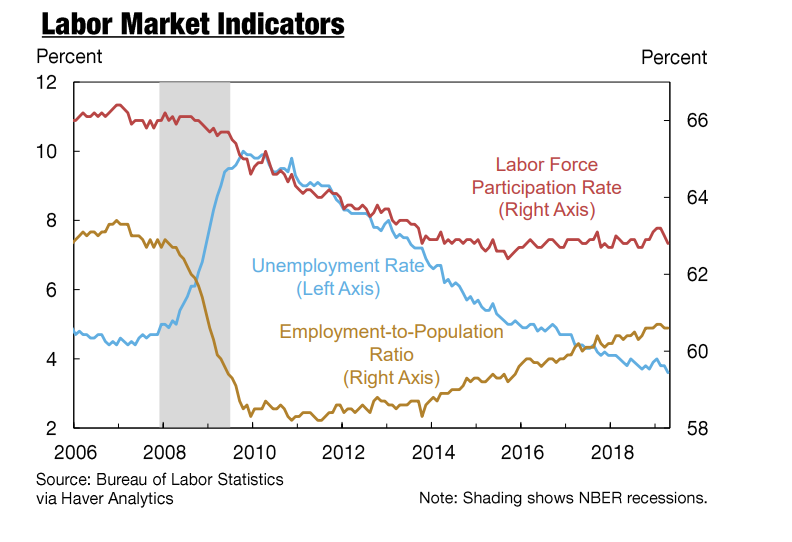

The job market is strong. At 3.6 percent, the unemployment rate is now lower than it was before the crisis. At 80 percent, the employment rate for workers in their prime working-age years—a more comprehensive measure of slack that includes shifts in labor force participation as well as unemployment—has recently risen close to its pre-crisis level.

就业市场的表现很强劲。目前的失业率为3.6%,低于危机前的水平。壮年劳工的就业率高达80% - 这一指标涵盖劳动参与率和失业率变化在内,是更为全面的衡量经济松弛程度的指标 - 最近已触及危机前的水平。

译者附图:美国的劳动参与率、失业率与就业人口比率(来自纽联储)

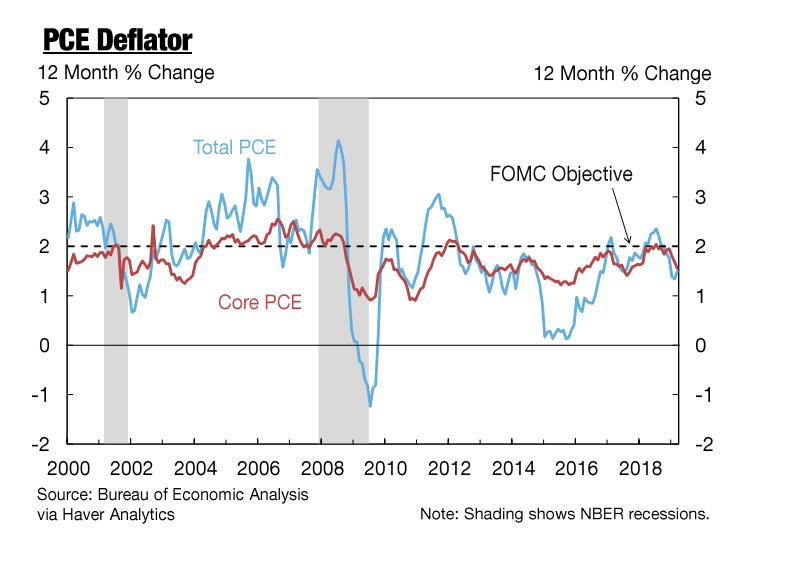

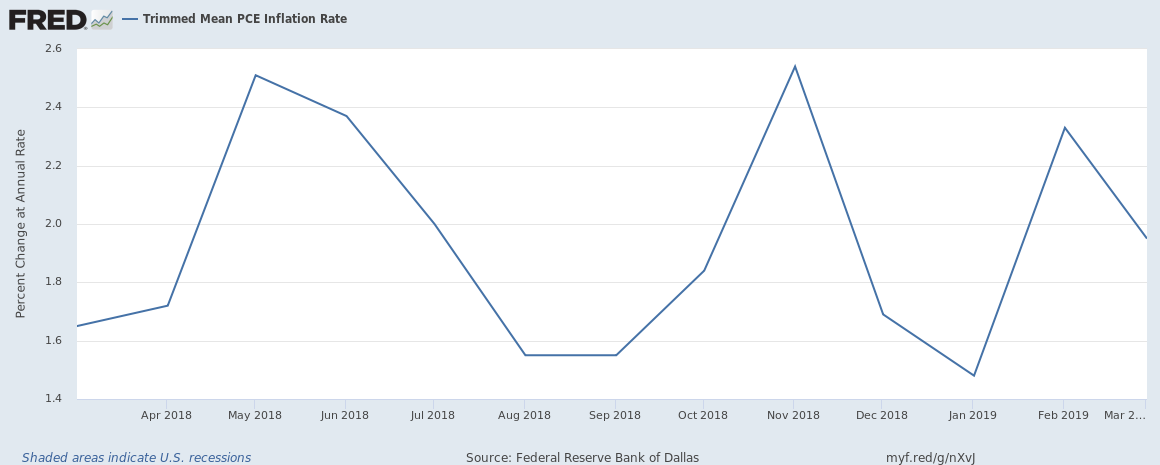

In contrast, the picture on inflation is puzzling this far into an expansion. Despite the strengthening of the labor market, the measure of core inflation excluding volatile food and energy prices did not move up to 2 percent on a sustained basis until last year, and in the most recent reading, the 12-month change has moved down to 1.6 percent. Other inflation measures paint a somewhat more reassuring picture. The Dallas Fed's trimmed mean measure of inflation, which provides a different way to filter out idiosyncratic movements in various components of inflation, has increased 2 percent in the past 12 months, slightly higher than its level of 1.9 percent for the two previous years.

相比之下,扩张时期通货膨胀的走势则令人感到费解。尽管劳动力市场有所增强,但直到去年,剔除食品和能源价格的核心通胀指标并没有持续上升到2%,而在最近的数据中,12个月的变化已经下降到1.6%。其他通胀指标也让人感到更加放心。达拉斯联储的通胀指标——Trimmed Mean PCE,提供了一种不同的方法来消除各种通胀因素的特殊变动,在过去12个月中增长了2%,略高于前两年的1.9%。

译者附图:PCE通胀以及Trimmed Mean PCE

新常态

Since the Great Recession, there have been several changes in macroeconomic relationships, which I refer to as the new normal. Now is a good time to assess the characteristics of the new normal and what they mean for monetary policy. The emerging contours of today's new normal are defined by low sensitivity of inflation to changes in labor market slack, a low long-term neutral rate of interest, and low underlying trend inflation. Let me take each in turn.

自大衰退以来,宏观经济关系发生了一些变化,我称之为新常态。现下正是评估这一新常态的特征及其货币政策意义的好时机。当前新常态所展现的是通货膨胀对劳动力市场松弛程度变化的低敏感性,低长期中性利率和低潜在趋势通胀水平所决定的。让我依次来解析。

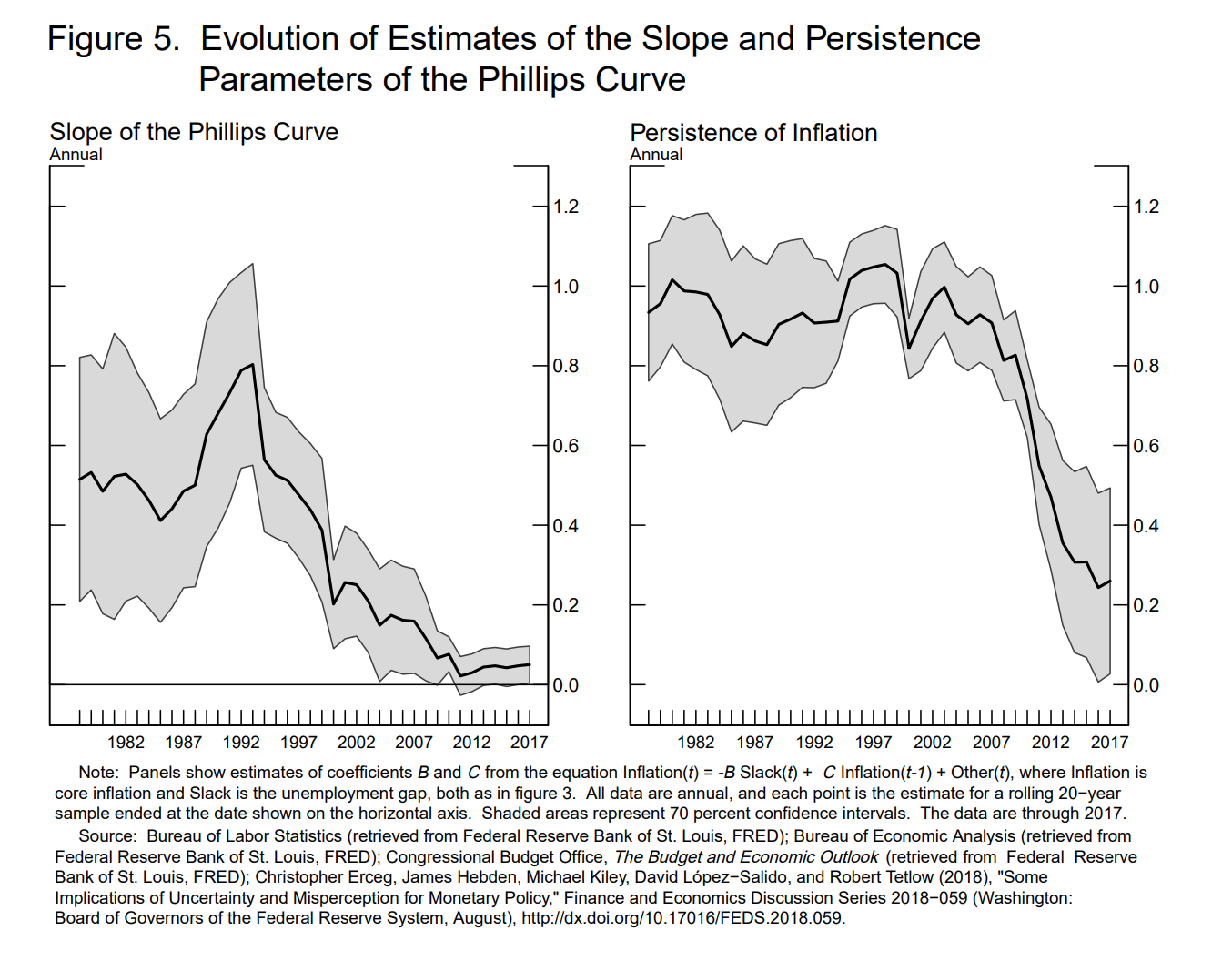

In today's new normal, price inflation has not moved up consistently as the labor market has strengthened considerably over the course of the long expansion. This is what economists mean when they say the Phillips curve is very flat: The historical relationship between resource slack and price inflation appears to have broken down. Although wage growth has been moving progressively higher as labor market slack has diminished, broader price inflation has remained muted.

在今天的新常态中,随着劳动力市场在长期经济扩张过程中大幅增强,价格通胀并未持续上升。这就是经济学家口中菲利普斯曲线平坦化的含义:资源松弛与价格通胀之间的历史关系似乎已经被打破。虽然随着劳动力市场的疲软程度下降,工资增长一直在逐步上升,但更广泛的价格通胀仍然保持低迷。

Another important feature of today's new normal is that the long-run neutral interest rate seems to be lower than it was historically. The neutral rate of interest refers to the level of the federal funds rate that would maintain the economy at full employment and 2 percent inflation if no tailwinds or headwinds were buffeting the economy. The decline in the neutral rate likely reflects a variety of forces globally, such as the aging of the population in many large economies, some slowing in the rate of productivity growth, and increases in the demand for safe assets. When one looks at the Federal Reserve's Summary of Economic Projections (SEP), it is striking that over the past five years, since the SEP interest rate projections first became available, the median estimate of the long-run federal funds rate has declined 1-1/2 percentage points, from 4‑1/4 percent to 2-3/4 percent. Going back further to the two decades before the crisis shows a similar decline in today's long-run neutral rate relative to earlier Blue Chip consensus forecasts of the long-run federal funds rate

今天的新常态的另一个重要特征是长期中性利率低于历史水平。中性利率指的是在没有任何阻力或不利因素影响经济,且将维持经济充分就业和2%的通货膨胀率的联邦基金利率的水平。中性利率的下降可能反映了来自全球的各种驱动力,例如许多大型经济体的人口老龄化,生产率增速有所下降,以及对安全资产的需求增加。如果我们看一看美联储的经济预测摘要(SEP),令人惊讶的是,在过去的五年中,自从SEP利率预测首次公开以来,长期联邦基金利率的中位数估计值下降了1.5%,从4.25%下降到了2.75%。回到危机前的二十年,相对于此前早期蓝筹共识预测中的数据,今天的长期中性利率出现了类似的下降。

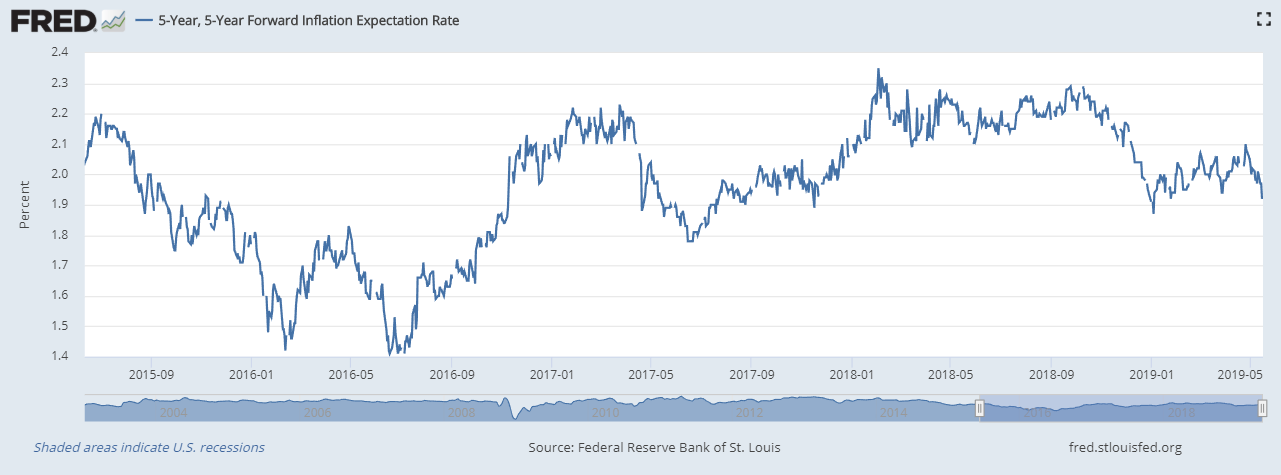

Third, underlying trend inflation—the trend in inflation after filtering out idiosyncratic and transitory factors—appears to be somewhat below the Federal Reserve's goal of 2 percent. This raises the risk that households and businesses could come to expect inflation to run persistently below the Federal Reserve's target and could change their behavior in a way that reinforces that expectation. Expectations are an important determinant of actual inflation because wage and price behavior by businesses and households is partly based on expectations of future inflation.

第三,潜在的趋势通胀 - 即过滤掉特殊和短暂因素后的通胀趋势 - 似乎略低于美联储2%的目标。这增加了家庭和企业可能会预期通胀持续低于美联储目标的风险,并可能改变其行为模式,进一步加强这样的预期。预期是实际通胀的重要决定因素,因为企业和家庭的工资和价格行为部分基于对未来通胀的预期。

译者附图:5y5y通胀预期

While low inflation and low interest rates have many benefits, the new normal presents a challenge for the conventional approach to monetary policy, in which the Federal Reserve could rely on changes in the level of the federal funds rate to achieve its inflation and employment goals. In past recessions, the Federal Reserve has typically cut interest rates by 4 to 5 percentage points in order to support household and business spending and hiring. With the long-run neutral rate low and with underlying trend inflation somewhat below target, nominal interest rates are likely to remain below those levels, which therefore leaves less room to cut rates as much as needed. With less room to ease financial conditions and support economic activity using our conventional policy tool, the economy may endure prolonged periods during and after recessions with short-term interest rates pinned at their effective lower bound. That, of course, was what happened following the financial crisis, when the Federal Reserve kept interest rates close to zero from December 2008 through November 2015.

虽然低通胀和低利率有许多好处,但新常态对传统的货币政策方法提出了挑战,即美联储可以依靠联邦基金利率水平的变化来实现其通胀和就业目标。在过去的经济衰退中,美联储通常将利率降低4至5个百分点,以支持家庭和企业的支出和招聘。时至今日,由于长期中性利率较低且潜在趋势通胀略低于目标,名义利率可能仍低于这些水平,因此联储的降息空间被缩小了。如若使用我们的传统政策工具来改善金融状况和支持经济活动的空间变小,那么,在经济衰退期间及渡过衰退期以后,短期利率会被锚定在其有效下限。这就是金融危机之后所发生的事情,当时的美联储从2008年12月到2015年11月之间一直将利率维持在接近零的水平。

That constraint limits the Federal Reserve's ability to provide stimulus through its conventional tool and thus could tend to leave inflation lower than it would otherwise be, and unemployment higher. The experience of several years with the federal funds rate pinned at its effective lower bound and actual inflation below our target could weigh on expectations for future inflation and thereby influence the behavior of households and businesses that helps determine wages and prices. The experience of a sustained period of low inflation could depress underlying trend inflation by feeding into lower inflation expectations, further reducing nominal interest rates and the space to cut interest rates in what could become a downward spiral.6 So we need to be especially careful to preserve as much of our conventional policy space as we can, while exploring mechanisms to augment the effectiveness of our framework.7

这种约束限制了美联储通过其传统工具提供刺激的能力,从而可能使通货膨胀率低于目标,且失业率更高。几年来,联邦基金利率被锚定在其有效下限叠加实际通胀低于联储目标的经验可能会影响对未来通胀的预期,从而影响有助于确定工资和价格的家庭和企业的行为。持续低通胀时期的经验可能会抑制潜在的趋势通胀,从而降低通胀预期,进一步降低名义利率以及美联储降低利率的空间。因此,我们需要特别谨慎小心地保留尽可能多的传统政策空间,同时探索增强框架有效性的机制。

新常态下的充分就业

The new normal has some important benefits. With subdued inflation, the sustained expansion has drawn workers back into the labor market after a damaging recession. The unemployment rate is approaching a 50-year low, and the overall labor force participation rate has remained constant despite the long-term aging of the population that would otherwise be pushing participation lower.

新常态有一些重要的好处。在通货膨胀较低的情况下,持续的经济扩张促使工人在经历了破坏性的经济衰退后得以重返劳动力市场。失业率接近50年来的最低水平,尽管人口持续老龄化,整体劳动力参与率仍保持不变。

Like the overall unemployment rate, broader measures of labor market slack are also lower than their pre-crisis levels. The Bureau of Labor Statistics' U-6 measure shows that two groups have recently shrunk to pre-crisis levels after rising considerably during the recession: those working part time who would prefer full-time employment and people marginally attached to the labor force who have looked for work in the previous year but stopped looking more recently. The strong labor market is leading to employment gains among workers with disabilities. Research suggests it may be helping to narrow some of the long-standing disparities for some racial minorities, although this development is tentative and modest

与整体失业率指标的走低一致,更广泛的衡量劳动力市场松弛程度的指标也低于危机前的水平。美国劳工统计局的U-6指标显示,两个统计组最近萎缩至危机前的水平:那些希望找到全职工作的临时工人,以及那些在前一年曾求职但近来不再找工作、即将退出劳动力市场的人群。强劲的劳动力市场正在导致残疾工人就业的增加。研究表明,这可能有助于缩小一些少数族裔就业长期存在的差距,尽管这种发展是暂时的且适度的。

We hear from business contacts that they are now hiring workers they may not previously have considered. During the recession, the evidence suggests that many employers raised their requirements for many job categories. As labor markets have tightened, employers in certain sectors, occupations, and areas of the country report they are loosening requirements and investing more in training. That means today's economy is providing opportunities for workers who might previously have been left on the sidelines—including those with records of past incarceration or who lack a particular certification or degree.

我们从商业联络人处获悉,他们现在正在招聘他们之前未曾考虑过的工人。在经济衰退期间,证据表明许多雇主提高了许多工作类别的要求。随着劳动力市场收紧,一些行业,职业和地区的雇主报告说他们正在放松要求并在培训方面投入更多资金。这意味着今天的经济为以前可能被抛弃的工人提供了机会 - 包括那些有过去监禁记录或缺乏特定证书或学位的人。

Given that the large majority of working-age households, those at the middle and lower ends of the income distribution, rely primarily on wage income, advancing our employment mandate has served the country well. In today's new normal, with the low responsiveness of inflation to labor market tightness, there appears to be little evidence so far of a tradeoff with our price-stability objective. The sustained strengthening of the labor market also adds to the productive capacity of the economy by attracting people on the sidelines to join or rejoin the labor force and move into employment.

鉴于绝大多数的劳动适龄家庭,即收入分布处于中下水平的家庭,主要依靠工资收入,推进我们的就业任务对国家有利。在今天的新常态中,由于通货膨胀对劳动力市场紧张的反应较低,到目前为止,没有证据表明需要在我们的价格稳定和就业目标之间做出权衡。劳动力市场的持续增强也通过吸引观望者加入或重新加入劳动力并进入就业,从而增加了经济的生产能力。

风险何在?

Of course, there are also risks. The past three downturns were precipitated not by rising inflation pressure, but rather by the buildup of financial imbalances. Extended periods of above-potential growth and low interest rates tend to be accompanied by rapid credit growth and elevated asset valuations, which tend to boost downside risks to the economy. It is not hard to see why a high-pressure economy might be associated with elevated financial imbalances, especially late in the cycle. As an expansion continues, the memory of the previous recession fades. Profits tend to rise, experienced loss rates on loans are low, and people tend to project recent trends into the future, which leads financial market participants and borrowers to become overly optimistic. Risk appetite rises, asset valuations become stretched, and credit is available on easier terms and to riskier borrowers than earlier in the cycle when memories of losses were still fresh.

当然,也存在风险。过去三次经济衰退的原因不是通胀压力上升,而是金融失衡的加剧。长期高于潜在增长和低利率往往伴随着信贷快速增长和资产估值上升,这往往会增加经济的下行风险。不难看出为什么高压经济可能与金融失衡加剧有关,特别是在周期的后期。随着经济扩张的继续,人们对过往经济衰退的记忆逐渐消退。利润趋于上升,贷款损失率低,人们倾向于将近期趋势预测延展到未来,这导致金融市场参与者和借款人变得过于乐观。风险偏好上升,资产估值高企,信贷可以更容易地被获得,人们失去了周期早期时对损失的审慎敏感性。

Historically, when the Phillips curve was steeper, inflation tended to rise as the economy heated up, which naturally prompted the Federal Reserve to raise interest rates. In turn, the interest rate increases would have the collateral effect of damping increases in asset prices and risk appetites. With a flat Phillips curve, inflation does not rise as much as resource utilization tightens, and, accordingly, provides less necessity for the Federal Reserve to raise rates to restrictive levels. At the same time, low interest rates along with sustained strong economic conditions are conducive to increasing risk appetites prompting reach-for-yield behavior and boosting financial excesses late in an expansion.

从历史上看,当菲利普斯曲线更加陡峭时,随着经济的升温,通货膨胀趋于上升,这自然促使美联储提高利率。反过来,利率上升会产生阻碍资产价格上涨和风险偏好的附带影响。而在菲利普斯曲线持平时,通货膨胀率不会随着资源利用率的增加而上升,因此,美联储不必将利率提高到限制水平。与此同时,低利率和持续强劲的经济条件有利于增加风险偏好,促使市场追求高收益,并在扩张后期推动金融过剩。

译者附图:美联储主席鲍威尔演讲中使用的菲利普斯曲线图表

With the forces holding down interest rates likely to persist, valuation pressures and risky corporate debt, such as leveraged lending, could well remain at elevated levels. Elevated valuations and corporate debt could leave the economy more vulnerable to negative shocks. The market volatility in December is a reminder of how sensitive markets can be to downside surprises.

由于拖住利率的力量可能持续存在,估值压力和高风险企业债务(如杠杆贷款)可能会保持在较高水平。估值上升和企业债务可能使经济更容易受到负面冲击的影响。12月份的市场波动提醒了人们市场对于下行意外的敏感程度。

A key implication of the weakening in the relationship between inflation and employment, then, is that we should not assume monetary policy will act to restrain the financial cycle as much as previously. As a consequence, policymakers may need to think differently about the interplay of the financial and business cycles due to the combination of a low neutral rate, a flat Phillips curve, and low underlying inflation. With financial stability risks likely to be more tightly linked to the business cycle than in the past, it may make sense to take actions other than tightening monetary policy to temper the financial cycle. In order to enable monetary policy to focus on supporting the return of inflation to our symmetric 2 percent target on a sustained basis along with maximum employment, we should be looking to countercyclical tools to temper the financial cycle.

因此,通货膨胀与就业之间关系减弱的一个关键含义是,我们不应该假设货币政策会像以前一样限制金融周期。因此,政策制定者可能需要对金融周期和商业周期的相互作用进行不同的思考,因为我们处于低中性利率,平坦的菲利普斯曲线和低潜在通货膨胀相结合的环境中。由于金融稳定风险与商业周期的关系可能比过去更紧密,因此采取紧缩货币政策以外的行动以缓和金融周期可能是有意义的。为了使货币政策能够集中力量支持通货膨胀恢复到我们对称的2%目标,并持续实现最大就业,我们需要考虑反周期工具来驯服金融周期。

One tool other central banks have been using to help temper the financial cycle is the countercyclical capital buffer (CCyB). The CCyB provides regulators with the authority to require large banks to build up an extra capital buffer as financial risks mount. Although the CCyB was authorized as part of the post-crisis package of reforms, so far, the Federal Reserve has chosen not to use it. Turning on the CCyB would build an extra layer of resilience and signal restraint, helping to damp the rising vulnerability of the overall system. Moreover, because the CCyB is explicitly countercyclical, it is intended to be cut if the outlook deteriorates, boosting the ability of banks to make loans when extending credit is most needed and providing a valuable signal about policymakers' intentions. This feature proved to be valuable in the United Kingdom in the wake of the Brexit referendum.

其他中央银行用来帮助缓和金融周期的一大工具是反周期资本缓冲(CCyB)。随着金融风险的增加,CCyB为监管机构提供了要求大型银行建立额外资本缓冲的权力。虽然CCyB被授权作为危机后一揽子改革的一部分,但到目前为止,美联储选择不使用它。启用CCyB将构建额外的弹性和信号抑制,有助于抑制整个系统日益增加的脆弱性。此外,由于CCyB是明确反周期的,如果经济前景恶化,它将被收回,提高银行在最需要信贷时提供贷款的能力,并提供有关政策制定者意图的有价值信号。在英国退欧公投之后,这一反周期特点在英国被证明是有价值的。

If countercyclical tools and other regulatory safeguards are not adequate over the cycle, monetary policy will need to carry a greater burden in leaning against financial excesses. That would be unfortunate, because adding financial stability concerns to the burden of conventional monetary policy might undermine sustained achievement of our employment and inflation goals.

如果反周期工具和其他监管保障措施在整个周期内不够充分,货币政策将需要承担更大的负担以抵御金融过剩。这将是不幸的,因为金融稳定性问题所增加的对常规货币政策的负担可能会破坏我们维持充分就业和通胀目标的努力。

Because the financial cycle is today likely to be tempered less than in the past by material increases in interest rates as the economy expands, the appropriate level of bank capital for today's conditions is unlikely to be the same as in past business cycles: Because interest rates likely will do less than in past cycles, regulatory buffers will need to do more. As a consequence, now is a bad time to be weakening the core resilience of our largest banking institutions or to be weakening oversight over the nonbank financial system. Instead, we should be safeguarding the capital and liquidity buffers of banks at the center of the system, carefully monitoring risks in the nonbank sector, and making good use of the countercyclical tool that we have.

由于随着经济的扩张,利率已经有所上行,当下的金融周期可能会比过去更加缓和,因此当前条件下适当的银行资本水平不太可能与过去的商业周期相同:因为利率可能会比过去的周期重要性更小,监管缓冲则需要做更多。因此,现在削弱最大的银行机构的核心弹性或削弱对非银行金融体系的监管不是一个好时机。相反,我们应该保护体系内核心银行的资本和流动性缓冲,仔细监控非银行部门的风险,并充分利用我们拥有的反周期工具。

在可持续的基础上实现我们的通货膨胀目标

Finally, let us turn to the apparent softness in underlying trend inflation. One hypothesis for the flat Phillips curve is that central banks have been so effective in anchoring inflation expectations that tightening resource utilization is no longer transmitted to price inflation.11 Another possibility is that structural factors such as administrative changes to health care costs, globalization, or technological-enabled disruption have been dominant in recent years, masking the operation of cyclical forces.12 Regardless, because inflation is ultimately a monetary phenomenon, the Federal Reserve has the capacity and the responsibility to ensure inflation expectations are firmly anchored at—and not below—our target.

最后,让我们转向潜在趋势通胀的明显疲软。平坦菲利普斯曲线的一个假设是央行在锚定通胀预期方面非常有效,以至于紧凑的资源利用率情况不再转化为价格通胀。另一种可能性是,近年来,诸如医疗保健成本的行政变化,全球化或技术破坏等结构性因素占据了主导地位,掩盖了周期性力量的运作。无论如何,由于通货膨胀最终是一种货币现象,美联储有能力和责任确保通胀预期牢固地固定在我们的目标上,而不是低于我们的目标。

As I have argued in the past, the fact that inflation has been running somewhat below our longer-run goal of 2 percent may not be entirely due to labor market slack or to transitory shocks; it also likely reflects some softening in inflation's underlying trend. First, estimates of underlying inflation based on statistical filters are lower than they were before the financial crisis and are currently below 2 percent. Second, estimates of longer-run inflation expectations based on the University of Michigan Surveys of Consumers and on inflation compensation from financial market pricing are also running lower than before the financial crisis.

正如我过去所说过的那样,通货膨胀率低于我们2%的长期目标可能不完全是由于劳动力市场的松弛或短暂的冲击所造成的; 这也可能反映了通胀潜在趋势的趋软。首先,基于统计过滤的潜在通胀估计值低于金融危机前的估计值,目前低于2%。其次,根据密歇根大学消费者调查和金融市场定价的通胀补偿,对长期通胀预期的估计也低于金融危机前的水平。

Our goal now is to get underlying trend inflation around our target on a sustained basis. What would this take? We can get some sense from statistical models. Although there is no one widely agreed-upon method of measuring underlying inflation, one statistical approach that has received attention in recent years captures the idea that underlying inflation responds to the experience with actual inflation, and that this responsiveness varies over time.15 We can use such an approach to get an idea of how much, and how quickly, underlying inflation might respond to any particular path for actual inflation. It provides some reassurance that our goal may be achievable if inflation moves only slightly above 2 percent for a couple of years. The SEP inflation projections of Committee members suggest that many have, over the past year or so, envisaged a few years of a mild overshoot.

我们现在的目标是在可持续的基础上围绕我们的通胀目标获得潜在的趋势通胀。这需要什么呢?我们可以从统计模型中来寻找。虽然没有一种广泛认可的衡量潜在通货膨胀的方法,但近年来受到关注的一种统计方法得出的结论是,潜在的通货膨胀对实际通货膨胀的经验作出反应,并且这种反应随时间而变化。我们可以使用这种方法来了解潜在通胀可能对实际通胀的任何特定路径做出多少和多快的反应。它提供了一些保证,即如果通胀在几年内略微超过2%,我们的目标可能是可以实现的。委员会成员的SEP通胀预测表明,在过去一年左右的时间里,许多委员会成员设想了几年的温和通胀超调。

Of course, it is not entirely clear how to move underlying trend inflation smoothly to our target on a sustained basis in the presence of a very flat Phillips curve. One possibility we might refer to as "opportunistic reflation" would be to take advantage of a modest increase in actual inflation to demonstrate to the public our commitment to our inflation goal on a symmetric basis.17 For example, suppose that an unexpected increase in core import price inflation drove overall inflation modestly above 2 percent for a couple of years. The Federal Reserve could use that opportunity to communicate that a mild overshooting of inflation is consistent with our goals and to align policy with that statement. Such an approach could help demonstrate to the public that the Committee is serious about achieving its 2 percent inflation objective on a sustained basis.

当然,如果在菲利普斯曲线非常平坦的情况下,如何在可持续的基础上顺利地将潜在的趋势通胀锚到我们的目标,目前尚不完全清楚。我们可能称之为“投机再通胀”的一种可能性是利用实际通货膨胀的适度增长来向公众展示我们在对称基础上对通胀目标的承诺。例如,假设核心进口价格通胀意外增加,导致整体通胀在几年内小幅上涨至2%以上。美联储可以利用这个机会表明温和的通货膨胀超调与我们的目标一致,并使政策与该声明保持一致。这种做法有助于向公众证明委员会认真对待持续实现其2%的通胀目标。

结论

In today's new normal, it is important to achieve inflation and inflation expectations around our 2 percent target on a sustained basis while guarding against financial imbalances through active use of countercyclical tools. We want to be mindful of the risk of financial imbalances that could amplify any shock and help tip the economy into recession, which the Federal Reserve has less conventional space to address in today's low interest rate environment. In my view, it is therefore wise to proceed cautiously, helping to sustain the expansion and further gains in employment and with appropriate regulatory safeguards that reduce the risk of dangerous financial imbalances.

在今天的新常态中,通过积极使用反周期工具来防止金融失衡,在可持续的基础上实现2%目标的通胀和通胀预期非常重要。我们希望时刻注意到金融失衡的风险可能会放大任何冲击,并导致经济陷入衰退,美联储在当今低利率环境下的常规工具空间较少。因此,我认为谨慎行事,有助于维持扩张和就业的进一步增长,并采取适当的监管保障措施,以减少危险的金融失衡风险。

声明:本文仅代表作者个人观点,不代表智堡立场;文中图片来源于网络,如有侵权烦请联系我们,我们将在确认后第一时间删除,谢谢!

0

推荐

京公网安备 11010502034662号

京公网安备 11010502034662号 {kind=link}